Streamlining the Student Eligibility Process

A meeting has been set with a new student to discuss their Financial Aid options. Before they arrive, you have some work to do.

You clack away on your keyboard and grab your trusty plastic log in token. It’s time to pull up NSLDS. Being a prepared FA Advisor you know it is better to review eligibility up front and deal with any issues head on.

You cross your fingers that the Enrollment Team gave you a valid social security number, and if you are lucky you already have an ISIR. You log into NSLDS at www.nsldsfap.ed.gov and pull the student’s NSLDS Summary. Here is what you are looking for.

- Warnings - Thankfully NSLDS believes in big icons and warnings at the top of the pages. Check for these big warnings at the top of the page. This is the first indicator your student is over their aggregate limits, in default, or has an overpayment.

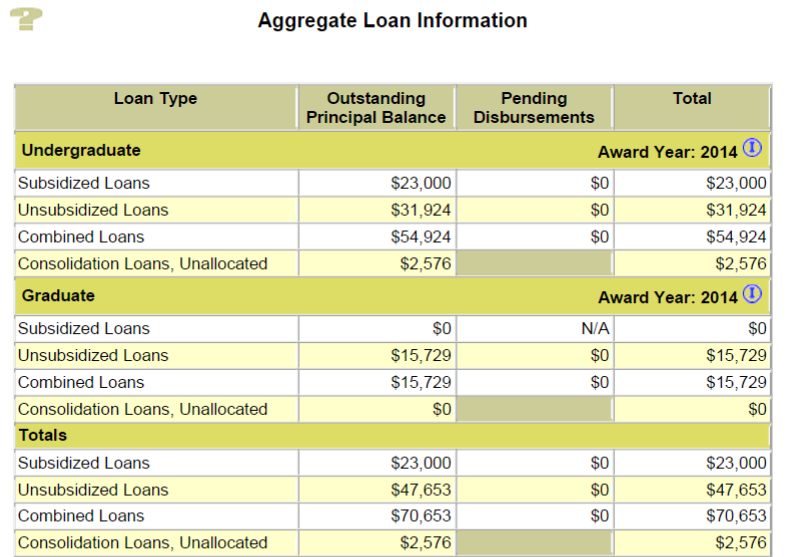

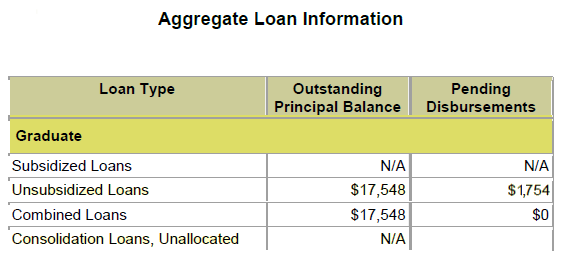

- Aggregate Limits - Did you remember to check both the undergrad and graduate aggregate limits? Don’t be fooled by only looking at one. Your student might be approaching their undergraduate aggregate limit and have a pending disbursement. If they are enrolled in a graduate program at your college you can’t ignore the potential over award for the undergrad amounts.

-

Pending Disbursements - Pending disbursements will affect eligibility. So, will ‘University of Slower than Dirt’ cancel this pending disbursement EVER?

-

Transfer Monitoring - So, your student has come from another institution. Oh the joys of Multiple Reporting Records situations that could possibly await you. No worries, you will add them to transfer monitoring to avoid any surprises that may affect future awards.

-

Check your Loan Status Codes - Check your status codes on each loan. Items that require extra care are Bankruptcy or Total and Permanent Disability (TPD) Discharges. You can see yourself blurting out into the office ‘Does anyone else remember if an AL status is ok?’

-

Loan Periods - Make sure prior loan periods don’t overlap the student’s academic year at your institution. Also check the length of the loan period. Is it shorter than an academic year? If so, it could be the short loan period was closing out an academic year from a prior loan. If that is not the case, then you will need to extend the loan period to a full academic year. Then check to see if the ‘new’ academic year overlaps.

So why are you doing this? Prescreening the NSLDS before the student arrives in the Financial Aid Office allows you to be proactive. It provides a road map of where you need to go and what needs to happen. After all, this proactive stuff may allow you to actually take a lunch today!

Additional Resources

Student Debts/Financial Aid History 34 CFR 668.35, 34 CFR 668.19, 34 CFR 668.32(g)(1), 34 CFR 668.32(g)(2), DCL GEN 96-13; DCL GEN 98-6; DCL GEN 01-09

NASFAA NSLDS Presentations:

http://slideplayer.com/slide/9816338/

http://slideplayer.com/slide/9453446/